Bartra Wealth Advisors have a limited number of final Irish Immigrant Investor Programme (IIP) approved investment slots available, with a restricted quota and timeframe. These slots are open to clients who have an immediate intention to apply for the IIP. Contact us now to secure your opportunity.

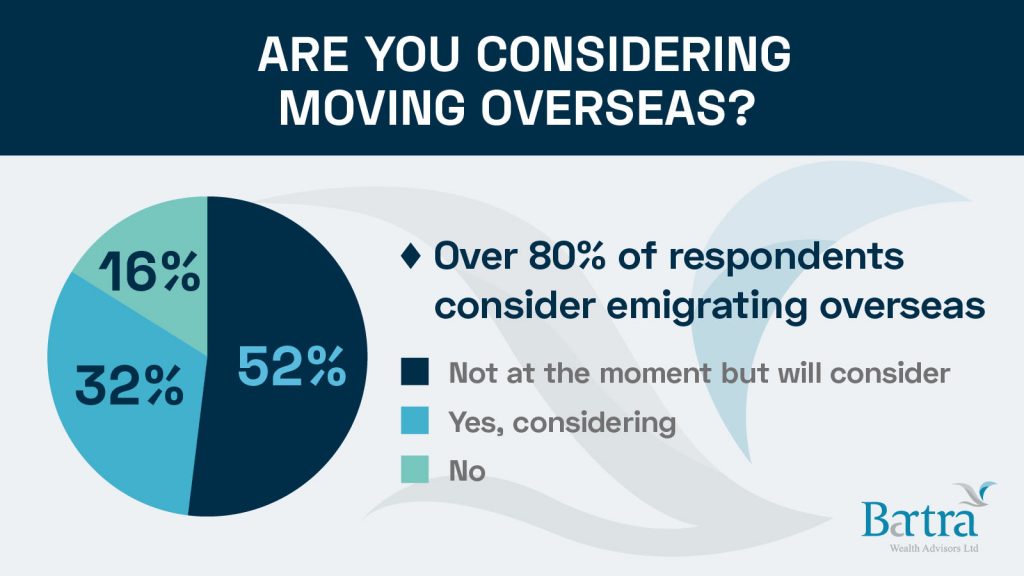

To understand the intent and views of the people of Hong Kong on emigrating overseas, Bartra Wealth Advisors (‘Bartra’), a subsidiary of Ireland’s market leading real estate developer and the first Irish immigration investment advisory in Hong Kong, conducted an online survey on emigration. From 1,200 responses, the survey found that 84% of respondents are currently considering or will consider emigrating overseas, among which the majority are high-income individuals including office workers, business people and professionals.

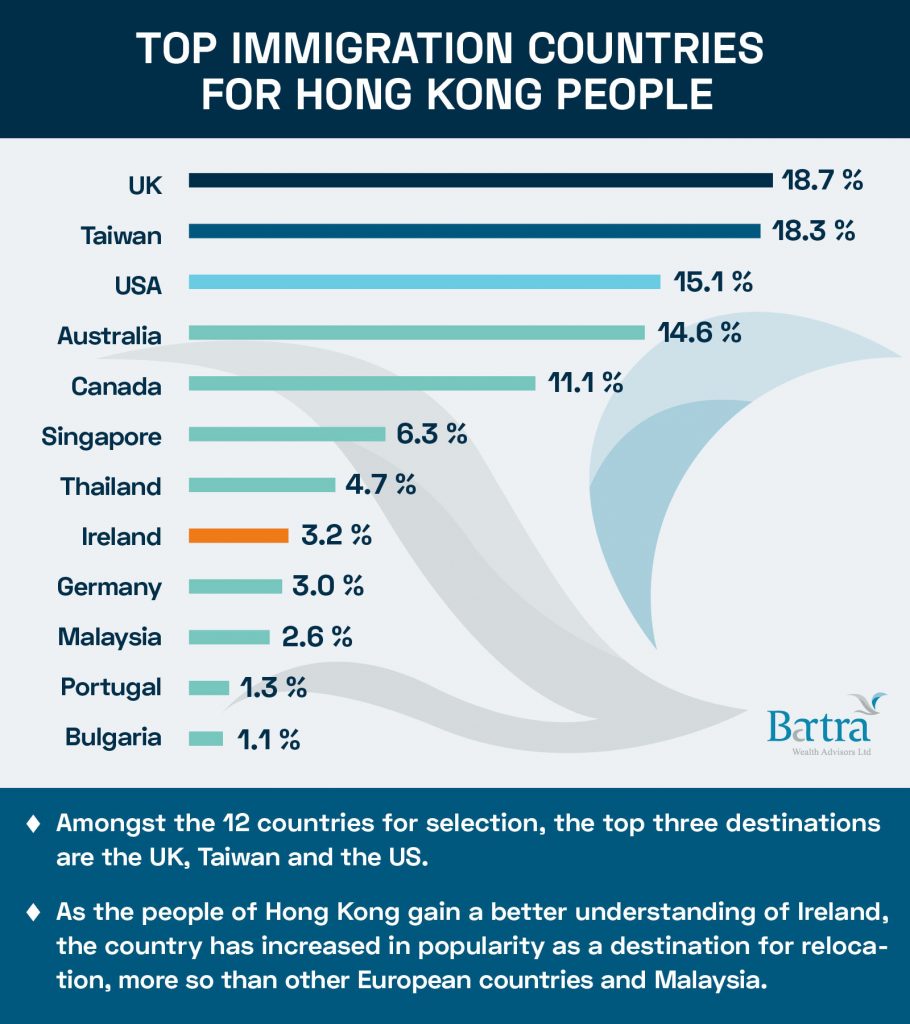

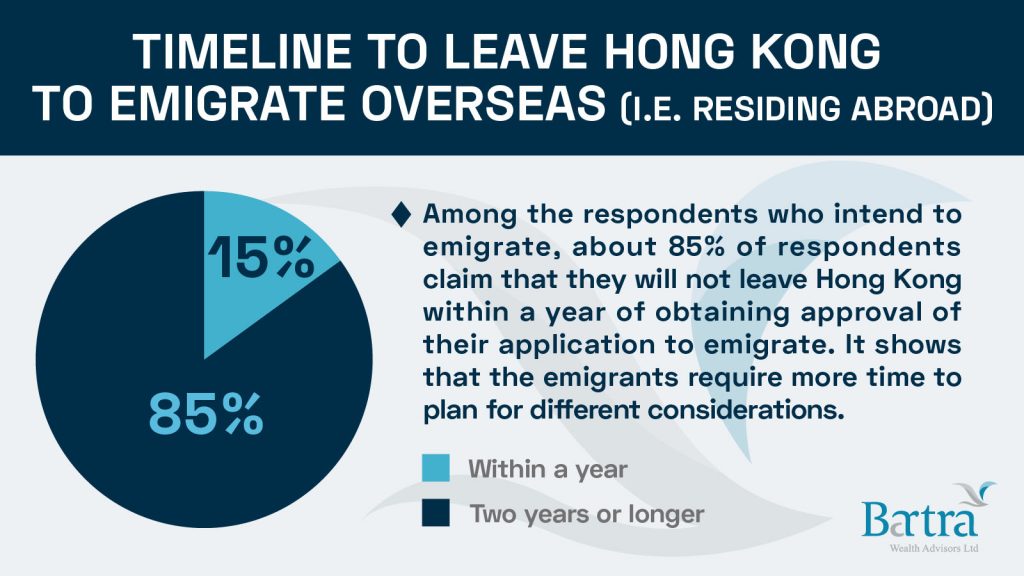

According to the survey, among the respondents who intend to emigrate about 85% of respondents claim that they will not leave Hong Kong within a year of obtaining an approval of their application to emigrate. The survey also found that over 50% of respondents’ decision to emigrate is in order to improve their living environment, while approximately 30% want their children to obtain a better education. To obtain a foreign residency/citizenship and political factors each account for 20%. As the people of Hong Kong gain a better understanding of Ireland, the country has increased in popularity as a destination for relocation, more so than other European countries and Malaysia. Currently, the top three destinations are the UK, Taiwan and the US. Meanwhile, the top three areas of concern for Hongkongers deciding to emigrate are the associated costs, the ease of application and language. Over 40% of respondents have considered obtaining residency by immigration investment, for which they care most about the security, return, and duration of the investment project, according to the findings of the survey.

Jeffrey Ling, Bartra Wealth Advisors Regional Manager, said, “Although the UK is still the top pick for relocation for the people of Hong Kong, uncertainty increased after Brexit which may affect the politico-economic environment in the UK. As a member of the European Union and part of the Common Travel Area with the UK, Ireland, an English-speaking country, is a gateway to both the UK and EU countries with promising business prospects; it is the first choice for many companies looking to relocate their headquarters. Moreover, this survey reveals that Hong Kong people require a great deal of flexibility around application and residency requirements via investment immigration, and they show a high degree of concern about the robustness and security of the investment projects. Both of these requirements are met by the Immigrant Investor Programme (‘IIP’) qualified projects that Bartra offers.”

Since the desire of high-net-worth clients to immigrate is strong and their top choice remains the UK, Bartra recommends they ensure a full understanding of the local investment market performance before immigrating. Wealth and investment management firm Harris Fraser was specially invited to conduct market analysis and share views on investment opportunities and wealth management trends. Cyrus Chan, Harris Fraser Investment Strategist, said, “With widespread vaccination programmes underway, the global economy is expected to recover faster than expected. However, although the UK and the EU came to an agreement for Brexit last year, relevant implementation details still need to be clarified. The troubled British economy may rebound, and the Irish economy will benefit from it. In addition, with the structural changes in the global economic environment, the wealth management needs of high-net-worth clients increase accordingly. Currently, more popular investment strategies include yield enhancement strategy, financial leverage, Euro asset allocation and focus on the healthcare sector.”

The pandemic has disrupted the relocation plans of many people in Hong Kong. According to the survey, Hongkongers require more time as well as a high degree of flexibility when planning for emigration. Jay Cheung, Bartra Wealth Advisors Marketing Director, said, “In the current climate, investment immigration services and products need to have three advantages: 1) high flexibility and fast-track process; 2) product safety and strong demand; 3) ability to add value and integrate with wealth management services.”

By investing in Ireland’s Immigrant Investor Programme (‘IIP’), application will be approved within 4-6 months, and applicants are only required to reside one day per year in Ireland to maintain their residency; in other words, they can obtain a foreign residency without relocating. Many of Bartra’s clients have already been granted permanent residency of Ireland, but have remained living and working in Hong Kong. In addition, Bartra commands unrivalled creditability in Irish immigration consultancy services. The Social Housing and Nursing Home projects Bartra offers to Hong Kong clients planning to obtain permanent residency in Ireland can be achieved in three or five years, and both guarantee 100% investment capital protection. They each have an approval and renewal rate of 100%. In addition, the Nursing Home project has an annual return of 4% paid on maturity, which is fitting of a high demand healthcare sector. As for the ability to integrate wealth management services, apart from cash, IIP applicants can use stocks, funds, cash value of insurance policies, properties, or even parking spaces and valuable paintings and collectibles etc., for asset requirement approval. Some clients will seek advice from financial services to pledge/refinance their assets to fund investment immigration in the current low interest environment so as to obtain residency without exiting from existing investments.

Pictures are Bartra’s press conference in early February.

The UK and the European Union (EU) finally agreed a deal on Christmas Eve that will define their future relationship. It replaces the partnership they have shared for the last 47 years. But will this take Brexit off the front pages or stop Brits talking about it? Or has the real Brexit battle only just begun? We have put together a summary of Brexit-related information to help you gain a better understanding of what the future holds for the UK and Europe.

What do we know about the deal?

The 1,246-page trade agreement has detailed provisions on many issues and contains new rules for how the UK and EU will live, work and trade together. Importantly, it means no tariffs or quotas will be introduced. However, while the deal came into force on 1 January, with everything left so late many people and businesses have not had much time to prepare for the changes.

There are four key things to be aware of:

1. Economy

The British government’s own fiscal watchdog, the Office for Budget Responsibility (OBR), has said that the deal will dampen long-term GDP by 4%, meaning Brexit is projected to do more economic damage to Britain than COVID-19. The deal is also seen as a ‘thin’ deal, which means it leaves many unresolved issues to be dealt with in later negotiations.

Yes, the UK has avoided tariffs on trade, but there will now be other complexities and mountains of paperwork. The UK benefited from access to more than 20 EU systems, which do everything from track the movements of goods and vehicles to store risk profiles for goods and producers from around the world, with the UK sharing its own data as part of this. But after Brexit, although tariffs for goods will be dropped, more friction may ensue as a result of other trade barriers, such as the administrative burden on traders, complicated border processes, and limited information sharing between customs authorities. Additionally, the new import and export declarations alone are likely to cost UK companies £7.5 billion ($10.3 billion) annually, according to HM Revenue & Customs.

Unemployment will also be a challenge post-Brexit. Since the June 2016 referendum, the job market has been contracting, with many companies leaving the UK, downsizing or cutting jobs. For example, in the financial services sector, Aviva, Britain’s second-largest insurer, stated that it would move £7.8 billion worth of assets to Ireland, while Bank of America Merrill Lynch (BAML) announced a merger between its UK and Irish subsidiaries, transferring 125 jobs to Dublin, which remains BAML’s European headquarters. Additionally, British bank Barclays is transferring £166bn of its clients’ assets to the Irish capital, while Credit Suisse plans to move about 250 bankers from London to other European financial hubs. According to EY, £1.2 trillion ($1.6 trillion) of assets, along with around 7,500 employees, have been transferred out of the UK to the EU, including to Dublin, Luxembourg, Frankfurt and Paris by financial services firms.

UK unemployment is forecast to reach 2.6 million by mid-2021, according to the government’s economic watchdog, which represents 7.5% of the working-age population. This will compound the impact of the COVID-19 pandemic, which has resulted in nearly 300,000 jobs lost in the hospitality sector since February 2020. In addition, retail has shed 160,000 jobs as non-essential shops have been forced to shut, and culture has seen 89,000 jobs go. And those figures are only for staff on company payrolls; thousands more casual workers and freelancers have been affected too. It seems unlikely that the UK’s economy will rebound quickly.

2. End of free movement

UK citizens and residents will no longer have the right to work, live, study or start a business in the EU without a visa, though short stays will be allowed (visa waivers will apply). This doesn’t help those seeking to travel frequently and do business in the EU. Comparing market capacity, the UK’s population is about 66.4 million, but the European Union’s, excluding the UK, is six times larger, which may lead to unfavourable business opportunities.

COVID-19 has also movement less free. The UK is Europe’s worst-hit country, with more than 40 countries banning UK arrivals in December 2020. There were hundreds of passengers at London’s Heathrow Airport scrambling onto the last flight to Dublin minutes before a travel ban set in at midnight on 20 December to nations across Europe. Tighter measures may apply with prolonged quarantine and pre-departure PCR tests likely required even when the situation begins to ease.

3. Education

Students and young people from Britain will no longer be able to take part in the Europe-wide Erasmus exchange programme. Since 1987, the Erasmus programme has provided opportunities for students to go on exchange abroad, linked schools across the EU and offered work experience and apprenticeships in European countries. Around 200,000 people, including 15,000 British university students, have participated in the programme in its latest incarnation.

Vivienne Stern, the Director of Universities UK International, told The Guardian, “As I understand it, there will be grants for young people not just in universities but broader than that, to support study and possibly working and volunteering. These experiences help graduates gain employment, especially for students from low-income backgrounds who are the least likely to be able to travel abroad otherwise.” She added that any Erasmus replacement needed to be “ambitious and fully funded”, and that it “must also deliver significant opportunities for future students to go global, which the Erasmus programme has provided to date.”

4. Financial services competitiveness

No deal has been agreed for financial services, which will be worrying for many would-be emigrants holding professional qualifications, particularly as these qualifications will no longer be mutually recognised between the UK and EU and professional persons will have to be separately registered in each.

The EU and UK have not yet struck a deal that will provide UK banks and asset managers with access to European markets. EU regulators are unlikely to allow London to keep the benefits of the single market without its obligations, and EU banks will have to cease from using platforms in the UK for swaps, certain derivatives and Euro-denominated stocks from January. UK financial services firms will lose their passporting rights, which in the past allowed them to sell funds, debt, advice, or insurance into the EU from their UK base without the need for additional regulatory clearances.

Worse, it means that UK firms have to agree and comply with the individual rules of each of the EU 27 Member States if they wish to sell financial services there. The implications for a loss of financial services activity from the UK to the EU are significant.

Due to Brexit, almost 30 financial groups have moved operations from London to Dublin. “We’re now seeing those financial services firms who have relocated, gained their licensing and are operationally ready, focus a lot more on ‘business as usual’,” said Cormac Kelly, financial services Brexit lead for EY Ireland in an interview with the Irish Times.

The post-Brexit trade agreement leaves many questions unanswered, but while there is uncertainty, there is likely also opportunity. Stay tuned for Part 2 of our Brexit and beyond article, where we look at what else lies ahead for the UK and the EU.

“By failing to prepare, you are preparing to fail” – Benjamin Franklin

We know how important making plans ahead of time can be, which is why we are publishing this piece now instead of waiting for the Brexit transition due to take place on 31 December. Here, we hope to share some insights with would-be immigrants currently looking at whether the United Kingdom should be their future home given the uncertainty surrounding Brexit and BN(O) citizenship.

Immigration is potentially the biggest decision that an individual or family will make in their life, and it’s complex. You need to understand your options, prepare and know what to expect on relocation.

The UK is considered a traditional immigration hotspot by Hongkongers. But is it the only option? The Republic of Ireland, Europe’s rising star, has been gaining traction internationally, with its capital, Dublin, an emerging financial centre and technology hub. In terms of GDP per capita, Ireland is ranked among the wealthiest countries in the Organisation for Economic Cooperation and Development (OECD) and the EU-27. It’s certainly a worthy contender for would-be immigrants to consider.

But first, a bit of background.

Strong Historical Links

For over a century and a half, from 1842 Hong Kong was a British colony before being handed back to China in 1997. And lasting legacies of this time endure in Hong Kong, particularly with regards to education, which is largely modelled on systems in the UK, specifically England.

As early as the 1100s, Ireland was ruled by the British, with some considering Ireland to be England’s first colony. Whatever its status, Ireland inherited much from the Brits, not least elements of its education system, which has evolved over the years and is now ranked 6th best in the world and is home to seven top-level universities.

Hong Kong people are, therefore, more familiar with Ireland than they might think. Hong Kong is also home to more than 6,000 graduates from Irish universities, and the education sector in Hong Kong has long-established Irish links; tens of thousands of people in Hong Kong have studied in Catholic schools run by Irish priests. Additionally, many of the colonial Governors of Hong Kong were born in Ireland or claimed Irish heritage, as were civil servants, police and judges from throughout Hong Kong’s colonial past. Today, many Irish business people, teachers and other professionals continue to build strong ties between Hong Kong and the Emerald Isle.

Education Matters

Education is of prime importance to parents, with early childhood education instrumental in a child’s social and intellectual development. In both the UK and Ireland, once residency is obtained children of applicants are able to enjoy free education and free choice of schools.

Some Hong Kong parents prefer that their children study in private schools where the student-to-teacher ratio is often lower, allowing teachers to spend more time on average with each student. However, with a smaller population in Ireland than in Hong Kong or the UK, both public and private schools offer small classes.

When it comes to comparing the ‘style’ of education, the Irish government pays more attention to personal development than schools in Hong Kong tend to, and students have less pressure when it comes to academic studies. However, Ireland believes that education is closely related to national planning, and vigorously promotes science, technology, engineering and mathematics education, with a vision to make Ireland an international centre for technology, science and financial services. Although some parents may send their children to top universities in the UK on completion of secondary education in Ireland, many have come to realise that Ireland has just as much to offer as England’s finest further education institutions such as Cambridge or Oxford. To learn more, take a look at our article on the many strengths of the Irish education system.

Trinity College Dublin, the University of Dublin is Ireland’s leading university, ranked No. 1 in Ireland and 101st in the world

So what are the options for those considering immigration and what costs and requirements are involved?

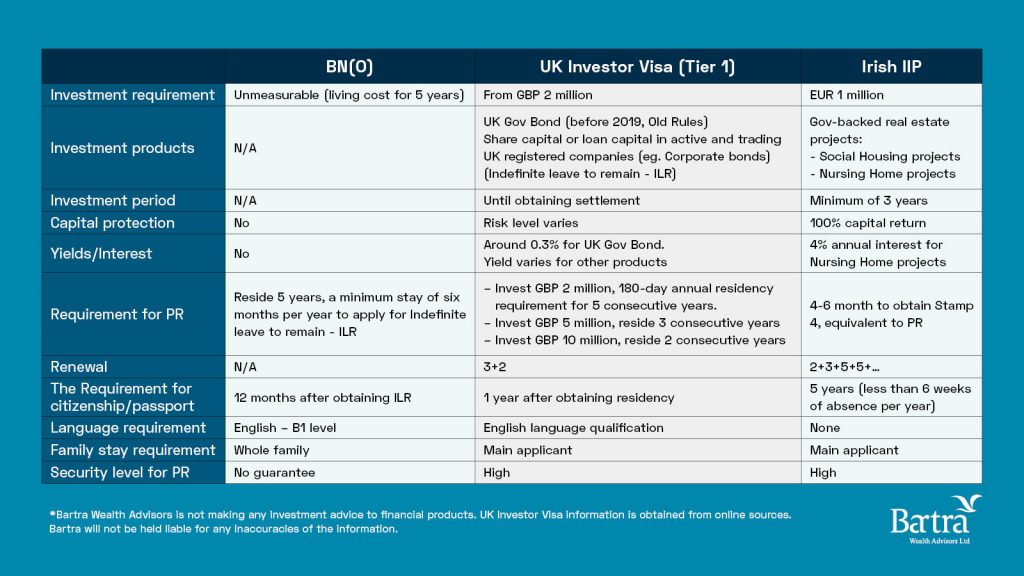

UK BN(O), UK Investor Visa and Irish IIP

UK BN(O)

For a BN(O) visa application, there is no direct cost or investment amount required. Expenses will be based on the costs of living for the whole family for at least five years. It’s important to pay attention to the restrictions of this option, as the whole family is required to reside in the UK to maintain residency. Additionally, BN(O) residents in the UK are restricted from accessing public funds. In most circumstances, BN(O) residents will not be able to enjoy social benefits, but will still be liable to taxes and national insurance. It is also worth noting that the UK is reviewing its Capital Gains Tax, which may usher in higher taxes or cut tax exemption.

UK Investor Visa

HNWIs seeking a residency visa for the UK can consider the Tier 1 Investor visa. The investment entry level is GBP 2 million, which is comparatively lower than the investment fund required by similar programmes in, for example, Australia or New Zealand.

Successful applicants will be granted a Tier 1 Investor visa initially valid for 3 years. The Tier 1 Investor visa can be extended for an additional two years as long as the main applicant does not spend more than 180 days outside the UK per year. It can also lead to UK permanent residency if the holders are able to meet the annual residency requirement for five consecutive years and maintain the investment fund.

Irish IIP

The Irish IIP is a cost-minimised immigration approach to obtain a foreign residency. It requires a EUR 1 million investment into INIS-approved projects for a minimum 3-year investment period to receive a Residence Permit (in the form of a Stamp-4 visa) upon approval. There a number of options for investment, but the Enterprise Investment route is the most popular. Bartra offers two Enterprise Investment options, Social Housing and Nursing Homes, both of which are safe and government-backed. The Social Housing scheme has a 3-year investment period with 100% repayment and no interest offered, while the Nursing Homes scheme is a 5-year investment with a 4% annual return (paid on exit), and 100% capital protection. The income from these projects is derived from a Sovereign Government, which is often described as ‘recession-proof’, even when taking into account external factors such as Brexit or global recession.

Transferability and Recognition

The Irish IIP is a straightforward immigration approach where applicants can receive permanent residency in one step, unlike for other immigration programmes where visas are initially only granted for temporary stay. The IIP has no travel restrictions to maintain residency status – just one-day residency in Ireland per calendar year is necessary. It provides flexibility and allows people to have a residency without moving, so there is no necessity to give up current jobs or businesses. This residency is later transferred to citizenship through naturalisation, which can be started at any time.

The Irish passport is the joint sixth strongest in the world, based on the number of countries its holders can visit visa-free. Its ranking is ahead of the US, the UK, Belgium, Switzerland and Norway, and it is the only passport in the world to provide both EU citizenship and the right to reside and work in the UK.

Comparatively, the BN(O) Visa offers five-year temporary residency, while a minimum stay of six months per year in the UK is required to maintain this residency status and there is no guarantee of transferability to permanent residency or citizenship at a later stage. It is also worth mentioning that the Chinese government is considering a ban on the use of the BN(O) passport as a legal travel document.

Similarly, the Tier 1 Investor visa requires that the applicant spend no more than 180 days absent from the UK in any 12 month period for 5 consecutive years in addition to the GBP 2 million investment. With an investment of GBP 10 million, two consecutive years with the same annual residency requirement are required.

The IIP investor and his/her family will be granted a Stamp 4 Visa, which is top-class immigration status. The immigrant also benefits from the added flexibility of being able to hold this status and enjoy social welfare benefits without having to reside in Ireland. Stamp 4 Visa holders’ children can enjoy free primary and secondary education and will pay the same university school fees as locals.

The BN(O) Visa is simply a means to work and reside temporarily in the UK. These immigrants have no access to social welfare benefits and its holders are often described as second-class citizens, which is an important element to bear in mind as quality of life should be a key consideration when weighing up options.

A Client Case Study

Bartra Wealth Advisors has received more than 1,600 enquiries related to immigration to Ireland in the past three months. Since August 2019, we have helped more than 50 families from Hong Kong successfully apply for Irish residency.

Jeffrey Ling, Regional Manager at Bartra Wealth Advisors in Hong Kong, shared one client story. Peter and May (both pseudonyms) are married with three children attending elementary school in Hong Kong. High-income, senior professionals, the couple had purchased properties in Hong Kong for investment purposes. They were keen to send their children (or go with their children) overseas to study, with a preference for an English-speaking country. However, their biggest concern regarding immigration was that they may not be able to find a job with a similar level of income after relocation, especially considering the current challenging times. The flexibility of the IIP was attractive, as it allows them to keep their jobs in Hong Kong while also obtaining residency overseas. In addition, due to its minimal residency requirement, they are considered non-Irish tax residents residing for fewer than 183 days a year, so there is no fear of double taxation. With its stable economic environment, strong legal system, world-class education, and accessibility to both the UK and EU, the couple felt that Ireland and the IIP fit their needs perfectly. The Advisory Agreement was signed with Bartra predominantly because the Enterprise Investment option we provide offers 100% capital protection with transparent and clear investment procedures. To find out more about the IIP and the projects we offer, start by reading our article The 4 Things You Must Know About the Ireland Immigrant Investor Programme.

In a recent webinar with South China Morning Post, we compared investment and immigration opportunities in the UK and in Ireland. Guest speakers included Liam Baily, Global Head of Research at Knight Frank; James Hartshorn, CEO and Co-Founder at Bartra; and Cheryl Arcibal, business and property journalist at South China Morning Post.

We hope this article provides you with the information you need to weigh up the available options and consider what works best for you and your families in terms of cost, requirements and quality of life.

Look out for upcoming articles where we’ll be comparing the economy and property markets in the UK and Ireland. If you have any questions or would like to find out more about the IIP, feel free to contact us directly.

Book an appointment to speak with one of our consultants.